Watching new records being set on the stock market and all the investment advisor enthusiasm, I can’t help remembering 2007 – the ‘calm before the storm’ of 2008 – and seeing some very direct parallels. Furthermore, Congress has reached a ‘budget deal’ – but one that continues to increase US government spending. The lame excuse offered is that “Federal outlays are still poised to grow from year to year, but at a slower pace than they would have without the efforts of budget hawks”.

Would someone please tell me how it can possibly be a good thing that US government expenditure is still increasing, in the light of the economic realities illustrated below? (We discussed them last month.)

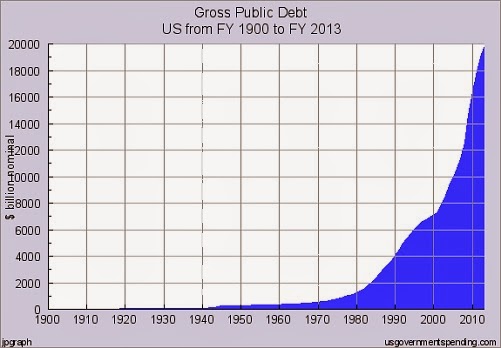

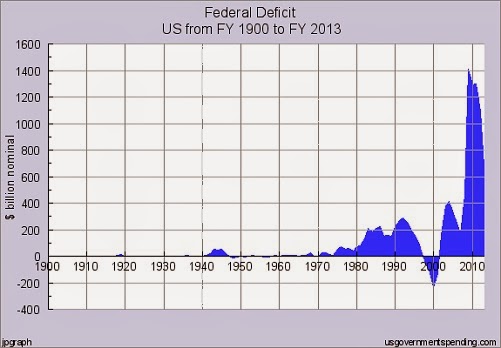

The ‘budget deal’ and the record stock market valuations fly directly in the face of the economic reality revealed by these three graphs. It’s utter madness to suggest anything else. Renowned investor Marc Faber puts it very clearly.

You can watch a longer version of that interview here. Highly recommended viewing.

As for what Mr. Faber says about bond interest rates, he’s absolutely right that when they increase again (as they inevitably will), it’s going to be very bad news indeed. We discussed this in four articles last August. Karl Denninger sees a more sinister side to the issue.

The Fed will cease QE on schedule. The taper is not only on, it won’t be suspended. And, withdrawing liquidity, that is, allowing short rates to rise, is on the table too, and almost-certainly sooner than you think.

. . .

If you remember I have repeatedly pointed out the utter insanity of QE in the first place. It is much like snorting heroin — you get a high immediately but the price is spread out.

. . .

So let’s say the effect of QE is that your mortgage goes from 6% to 3%. This is a 50% reduction in your interest payment. But — that MBS gets sold into the market. MBS have a typical maturity profile of about 7 years (which is why the 10 is the benchmark; it’s the closest), fluctuating somewhat. When rates are high and falling the profile is shorter (because people refinance), when rates are low and going higher it extends (because you’re a nut to refinance a 3% loan into a 4% one — nobody does that unless you have to sell and move for some reason.)

So the guy who buys it gets a 50% reduction in his interest income, but that’s only 1/10th of his portfolio. For the first year, anyway. As such his impact the first year is 5%, then 10%, then 15% and so on.

We’re roughly five years into this crap now.

The pension funds and insurance companies that are the backbone of this market are probably doing plenty of screaming, and with good cause. If this keeps up their cash flow will collapse; they can’t absorb it. Further, Bernanke and the rest of the Fed know that factually the damage they took on by buying those instruments during QE cannot be gotten rid of either; it has to roll off, because if you sell that bond you’re going to take a capital loss and crystallize the entire loss right now instead of spreading it out!

This is what is forcing the end of QE. It is also what is going to force The Fed to pull liquidity and let the short end come up.

There’s more at the link. Recommended reading.

I believe the economy is teetering right on the brink of a major reversal, just as it was in 2007 and early 2008. The head of steam it’s built up in recent months, thanks to the surplus liquidity generated by QE, is not underpinned by substantial or worthwhile fundamentals. International danger signals are flashing. To take just one glaring example, Zero Hedge reports a 40% collapse in the Baltic Dry index (which measures ship cargo costs), and warns that “While this is the worst start to a year in over 30 years, the scale of this meltdown is only matched by the total devastation that occurred in Q3 2008”. This index measures, in effect, the demand for shipping to move goods to and between markets. If the volume of goods shipped is collapsing, what does that say about the economies that are no longer ordering them? And that’s only one of the indicators that scares the hell out of me, and other knowledgeable observers.

Still happy about those stock market figures?

Peter

I personally prefer the "debt as a percentage of GDP, adjusted for inflation" charts. They don't look as bad, but they also are much harder to dismiss as mere scary statistical chart tricks by scare-mongers. Economic growth has been >10x in real terms in the last century, and inflation stolen >95% of the value of the dollar, so the chart misrepresents the case by roughly 99.5%. It's still ugly, but it's not THAT ugly. Faber always has good things to say, even when he repeats himself. I, too, think we are close to some major events (blow-up, melt-down, bail-out, "unexpected" executive action).