We need to be paying closer attention to what’s happening beneath the surface of the housing market. It’s beginning to look a lot like 2007.

On the surface, things look great. We see headlines such as:

- Millennials Help Sustain Twin Cities Housing Market Boom

- Real estate CEO: Record-low housing inventory is ‘freaking us out’

- Houses selling fast: ‘If you wait, boom it’s gone’

- Building to a boom: Subdivisions filling in quickly as real estate market rebounds

However, below the surface, there are worrying signs – and they have to do with buyers, not sellers. Two articles in recent weeks have caught my eye. The first is titled “Run-up in home prices is ‘not sustainable’: Realtors’ chief economist“.

“The continuing run-up in home prices above the pace of income growth is simply not sustainable,” wrote Lawrence Yun, chief economist for the National Association of Realtors, in response to the latest price reading from the much-watched S&P CoreLogic Case Shiller Home Price Indices. “From the cyclical low point in home prices six years ago, a typical home price has increased by 48 percent while the average wage rate has grown by only 14 percent.”

Yun also pointed to rising mortgage interest rates as a factor that would weaken affordability. The average rate on the 30-year fixed mortgage is nearly a full percentage point higher today than it was at its most recent low in September 2017.

. . .

Meanwhile the home price gains are widest on the low end of the market, where supply is leanest. That is why home sales have been dropping most on the low end. Evidence is now mounting that a growing number of first-time buyers are giving up and dropping out of the market altogether. Sales to first-time buyers dropped 2 percent in the first quarter of this year compared with the first quarter of 2017, according to Genworth Mortgage Insurance.

There’s more at the link.

Mr. Yun makes a very important point. For those who are relatively wealthy, the increase in housing prices over the past few years has been inconvenient; but for those living on limited incomes, it’s been disastrous. The lack of affordable “starter homes” has also been getting worse, as builders focus on providing more expensive houses on which their profit margin is higher. On the street where Miss D. and I live, where most houses are smaller units in the 1,300-1,500 square feet range, prices have shot up by 20%-30% since we moved in, two and a half years ago. That’s driven purely by demand, because the homes on this street are relatively good-quality, largely “move-in-ready” brick buildings, offering a lot compared to others in their price range, so that demand remains high. However, less desirable buildings nearby, at a lower price, are hard to move, because banks will finance their purchase price, but are reluctant to grant increased mortgages to pay for their upgrading.

That brings us to the second article, titled “The Headwind Facing Housing“. Here’s an excerpt. Bold, underlined text is my emphasis.

In 1981 mortgage rates peaked at 18.50%. Since that time they have declined steadily and now stands at a relatively paltry 4.50%. Over this 37-year period, individuals’ payments on mortgage loans also declined allowing buyers to get more for their money. Continually declining rates also allowed them to further reduce their payments through refinancing. Consider that in 1990 a $500,000 house, bought with a 10%, 30-year fixed rate mortgage, which was the going rate, would have required a monthly principal and interest payment of $4,388. Today a loan for the same amount at the 4.50% current rate is almost half the payment at $2,533.

The sensitivity of mortgage payments to changes in mortgage rates is about 9%, meaning that each 1% increase or decrease in the mortgage rate results in a payment increase or decrease of 9%. From a home buyer’s perspective, this means that each 1% change in rates makes the house more or less affordable by about 9%.

. . .

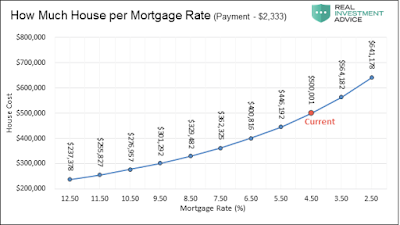

To put this into a different perspective, the following graph shows how much a buyer can afford to pay for a house assuming a fixed payment ($2,333) and varying mortgage rates. The payment is based on the current mortgage rate.

. . .The consequences of higher mortgage rates will not only affect buyers and sellers of housing but also make borrowing on the equity in homes more expensive. From a macro perspective, consider that housing contributes 15-18% to GDP, according to the National Association of Home Builders (NAHB).

. . .

Rising rates not only impact affordability but also the general level of activity which feeds back into the economy. In addition to the effect that rates may have, also consider that the demographics for housing are challenged as retiring, empty-nest baby boomers seek to downsize. To whom will they sell and at what price?

If interest rates do indeed continue to rise, there is a lot more risk embedded in the housing market than currently seems apparent as these and other dynamics converge. The services providing pricing insight into the value of the housing market may do a fine job of assessing current value, but they lack the sophistication required to see around the next economic corner.

Again, more at the link. Highly recommended reading.

The second article graphically illustrates the challenge facing many older Americans. Many of them have invested in large, comfortable houses, but made little or no provision for retirement funding. They expect to sell their homes for a considerable profit, and use that profit to bankroll their retirement. However, if housing prices fall rather than rise, and/or new buyers can’t obtain mortgage financing for those large, comfortable houses because they can’t afford the monthly repayments at higher interest rates, what are the owners going to do? The same factors that make mortgages more expensive for prospective buyers will probably restrict or even prevent them from taking out home equity loans secured against their houses, because – on their newly-reduced retirement income – they won’t be able to afford the higher payments, either!

The current headlines about the housing “boom” seem very comforting and reassuring. However, below the surface, I’m seeing more and more counter-currents. If I were buying right now, I’d hesitate to stick my toe in that water unless I had an ironclad guarantee that I’d be able to continue to afford the payments. That depends more on the job market than anything else – and that market’s not looking great for the long term. More and more part-time workers, who earn less money: more and more automation where robots and artificial intelligence systems replace (expensive) full-time employees . . .

That’s not a happy thought. Mish Shedlock sums it up thus. Again, bold, underlined text is my emphasis.

Among other effects, debt boosts asset prices. That’s why stocks and real estate have performed so well. But with rates now rising and the Fed unloading assets, those same prices are highly vulnerable. An asset’s value is what someone will pay for it. If financing costs rise and buyers lack cash, the asset price must fall. And fall it will. The consensus at my New York dinner was recession in the last half of 2019. Peter expects it sooner, in Q1 2019.

If that’s right, financial market fireworks aren’t far away.

Peter

Re the inability of retirees to sell their houses to finance their retirements: Maybe we'll see an increase in the number of "reverse mortgages".

But the higher that interest rates are, the lower will be reverse mortgage payments, since in this case interest rates are actually discount rates.

IF there is a recession Trump will be toast in 2020.

I haven't had the income to sustain the purchase of a home in over a decade. And to be honest, renting has been a financial struggle the last few years and has gotten worse over the last year. I finally bit the bullet cashed in some of an inherited IRA; bought a tornado magnet so I could cut my housing costs to within my means, while still live in a 'decent neighborhood'.

I fully understand the price/interest rate relationship.

When my wife and I bought our first house, interest rates were ~8%. And our loan was, as I recall $146K. Since we only had a 10% down payment, we also had to pay PMI.

Six years later, we sold the first house and bought our current home. I was earning more, but was really worried about paying off our $300K mortgage. Until I realized that between the lower interest rates (just under 6%, as I recall) and having a 25% down payment (no PMI) our house payments were about the same.

Currently, mortgages are floating at roughly 4%. If they rise to 6%, I'd expect housing prices to drop by 10-20%, maybe more.

On the other hand, if you can manage to buy a house when the interest rates are high, you can do very well if the rates drop. You can often refinance for a 15 or even 10 year fixed-rate mortgage to replace your original 30-year mortgage, and reduce your payment at the same time.

I'll also point out that the federal tax deduction for mortgage interest is a LOT more valuable when interest rates rise. Not that it totally makes up for the higher payments. But it does make them a bit more tolerable.

Another thing that limits the supply of low-end/"starter" homes for sale: the price of land. This is especially important in markets where the availability of buildable land is limited, due to geography and/or legal constraints (zoning, "green space" laws, etc.)

The more it costs to acquire the underlying patch of dirt, the fancier/more expensive the house (or condos, or whatever) that the developers is going to build on it, in order to get a decent return on his money.

Increasing the costs for obtaining the necessary permits, etc (i.e. if the locality adds things like an "affordable housing tax" or other such thing) likewise increases the cost of the structure(s), again so the builder can make a reasonable profit.

(And places that are the most geographically constrained – such as San Francisco (water on three sides, cemetaries of Colma on the fourth) or Seattle (water on two sides) also seem to have the most aggressive limits on land use and biggest piles of expensive regulations and taxes.)

What Dave said applies to Silicon Valley, too. Bigger area than San Francisco, but when you take into account the non-build-able hillsides surrounding the valley floor (protected by law as open space) the Bay wetlands to the north (ditto), and the farmland to the south (again, open space) there is very little land left that isn't either already built on or zoned to limit housing.

Plus, in California, cities try to avoid building more housing because of Prop 13, which sharply limits property tax increases. Commercial development gives them business taxes, and (for retail) sales taxes. High-end residential may still bring in enough property taxes per household to cover expenses. Middle- and low- income housing barely covers expenses to the city when they're built – and after a few years, require more money in services than they return in taxes.

I'm currently benefiting from Prop 13, but it's had the unfortunate side effect of maximizing taxes for new homeowners (so the city can hope to recoup their cost) while subsidizing longer-term homeowners and businesses (and in this area, commercial property changes hands to trigger a new base assesed value much less often than residential proerty does). Yes, I'm very happy that my property tax has only increases by 2% per year for the last couple of decades – but the guy down the street who's just moving in will probably be paying nearly 3x as much per year in property taxes.

The local cities pay lip service to "affordable housing" – but what they really want is new retail, or corporate headquarters.

"That depends more on the job market than anything else – and that market's not looking great for the long term. More and more part-time workers, who earn less money: more and more automation where robots and artificial intelligence systems replace (expensive) full-time employees . . ."

According to Ms Hoyt and lots of other people, that's not happening because new and different jobs are being created to maintain the robots, etc.

Yeah, for those who can be retrained to do it. After that, you start having people moving into "service" jobs which are very much dependent on waiting on the whims of other people. The quality hiring serfs, is one way to put it.

Another significant factor in driving up the cost of new housing is that the building codes are requiring that the new houses be significantly 'better' houses, not just in terms of safety, but in terms of energy efficiency (an extreme example being the new California requirement to install solar panels on the house)

If you do enough modifications to an existing house, you are required to upgrade it to meet the new codes.

In addition, you have a large number of people who are buying houses as an investment, and so are snapping up the cheap houses and then renting them out. This further reduces the number of houses available.

add to this the 'no/slow growth' movements in many areas (especially urban areas) and it's not at all surprising to see that getting started is hard.