A couple of days ago we examined the bond market and the clear and present danger to our economy posed by rising interest rates. I’ve had a couple of folks ask me why that’s such a problem, when if worst comes to worst we can simply ‘do a Detroit’ and declare bankruptcy. This article is an attempt to address that perspective.

First, if interest rates rise, it’ll threaten the investments of millions of ordinary people (particularly retired persons who rely on the income stream from their investments to survive). In the absence of ‘real’ interest rates (i.e. an interest rate that exceeds the rate of inflation), many people have turned to the stock market, housing, or many other classes of assets, in an attempt to invest their money in something that will appreciate in value. You’ll remember that I pointed out the inverse relationship between bond prices and interest rates: usually, when one goes up, the other goes down. That’s what’s driven the rising prices of assets such as stocks and shares over the past few years. Money has flooded into the stock market because interest rates were dropping, so there was almost nowhere else it could earn a return exceeding the rate of inflation. That’s probably about to change. As the Telegraph points out:

Ben Inker, the co-head of asset allocation at GMO, a giant American asset manager, said the US Federal Reserve’s policy of low interest rates had boosted the value of almost all assets and that any expectation that rates would rise risked triggering a reversal.

When returns on cash are low, investors switch to other assets in the search for higher income. This increased demand pushes up prices.

“By pulling down both today’s cash [interest] rate and the market expectation of future cash rates, the Fed has increased the relative attractiveness of pretty much all assets other than cash and, as a consequence, their prices have risen,” Mr Inker wrote in a recent research note.

“Since 2009 it has been difficult to avoid making money in the financial markets. Conventional bonds, inflation-linked bonds, commodities, credit, equities, real estate – everything – has been bid up as a consequence of the very low expected returns of cash.”

But he warned that this gave today’s markets “a vulnerability that has not existed through most of history”.

“Today’s valuations only make sense in light of low expected cash rates. Remove that expectation, and pretty much every asset across the board is vulnerable to a fall in price, as the rising real discount rate plays no favourites,” Mr Inker said.

He added: “We have known this for a while, but the trouble is that there is no easy way to resolve this problem. There is no asset class you can hold that would be expected to do well if the real discount rate rises from here.”

Under normal circumstances, rising rates would follow rising inflation or stronger than expected growth, which a diversified portfolio of investments could usually cope with, he said.

But recent fears of rate rises came not because inflation was unexpectedly high, or because growth will be so strong as to lift earnings expectations for equities and other owners of real assets, but “because the Fed signalled that there was likely to be an end to financial repression in the next few years”.

“Financial repression” means artificially low real (inflation-adjusted) interest rates imposed by governments as a means to reduce their own borrowing costs.

The effects of a change of direction are unlikely to be confined to America.

Mr Inker added: “Because financial repression has pushed up the prices of assets across the board and around the world, there is unlikely to be a safe harbour from the fallout, other than cash itself.

There’s more at the link. Important reading.

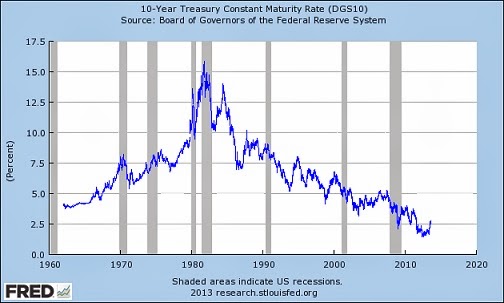

Karl Denninger points out the significance of the turnaround in interest rates – particularly for the housing market.

… the real issue is this one (click graphic for source):

This is a 30 year secular trend and it’s ending.

That is, the secular trend toward lower interest rates across the board.

Notice that every significant economic calamity since 1980 — 1987, the mid-1990s recession and debt problems, 2000, 2007 — all came about as the consequence of excessive leverage when the secular downtrend suffered a cyclical reversal.

There is a 100% correlation folks.

Now this secular trend is changing. It is changing because it must. It will either flatten out (less likely) or reverse, and as a consequence all of those economic behaviors, whether by governments, companies or individuals that have been profitable into a secular decline in rates will lose money.

Every one of them.

Again, more at the link.

Detroit has defaulted on its municipal bond obligations because its tax base has shrunk to the point that it can no longer collect enough in rates and fees to service its debt. That’s happening elsewhere in the country as well – for example, witness last month’s bond default by a Florida bridge agency. Note how many California cities have declared bankruptcy, or are seriously considering it. The contagion is spreading fast.

This increases the risk to investors in the bonds issued by such cities and agencies – so, inevitably, they demand higher interest rates to compensate them for the increased risk. Those issuing the bonds are obliged to pass on those higher interest costs to their users in the form of higher rates, fees and other charges. This has a ‘trickle-up’ effect, as local governments’ fiscal troubles affect regional governments, which affects state governments and the federal government in turn. Soon all of them will be obliged to offer higher interest to potential investors, otherwise no-one will buy their bonds. The exception – so far – has been the federal government, which has relied on the Fed to buy Treasury bonds at laughably low interest rates, because no private or sovereign investors have been prepared to do so. As we pointed out earlier, this means that in 2013 the Fed will have to buy more than 90% of Treasury bonds in order to keep the federal government afloat. It’s nothing more or less than a fiscal shell game. It damages our currency, it affects our standing in the eyes of the rest of the world, and it’s ultimately self-defeating.

The rise in interest rates that has already begun will inevitably drive down asset prices, as outlined above. That means that the Fed’s balance sheet may be seriously affected. Right now it’s carrying almost two trillion dollars’ worth of Treasury bonds on its books as assets, listed at their face value. If it has to ‘mark them to market‘ – i.e. list them at what others will actually pay for them right now – the value of its assets will show a serious decline. It’ll become technically bankrupt, and be unable to sell its assets for sufficient funds to deal with any other financial crisis that comes along. That means its only recourse will be to print yet more money – but it’s already pumped over $3 trillion of hyperinflationary excess cash into our economy. It can’t use that tactic much longer without risking a Weimar Republic-type disaster.

To those who wonder why the USA as a whole can’t simply ‘do a Detroit’ and declare bankruptcy in the face of this reality – think again. We are the economic powerhouse of the entire world. If the USA defaults, every other nation on earth is likely to follow suit. No-one will be repaid what they’ve invested; almost everyone will lose everything. The world financial system will descend into a dog-eat-dog, devil-take-the-hindmost, knock-down-and-drag-out brawl. There will be no financial security for anyone. Rising interest rates will be the least of our worries.

Do you really want to live in a world like that? You may get the opportunity . . .

Peter

Yep. With the current interest rates for savings, it certainly doesn't make any sense to keep your funds in a bank. You're better off putting them into tangible things that will increase in value, like copper, lead, and brass….