I’ve lost count of how many times I’ve warned of the perils of debt in general, and the national debt (i.e. what the US government owes) in particular. Deficit spending (the primary cause of the problem) is currently growing the national debt at almost $1 trillion per year, and it’s getting worse.

Prager University has just published this video, setting out in plain and simple terms why this is unsustainable, and must be stopped. I can’t recommend too strongly that you watch this all the way through, and then send the link to your family and friends. Unless all Americans unite around this issue very soon, the damage will span multiple generations. It’ll certainly impact all of our futures and all of our retirements, no matter how old (or young) we are.

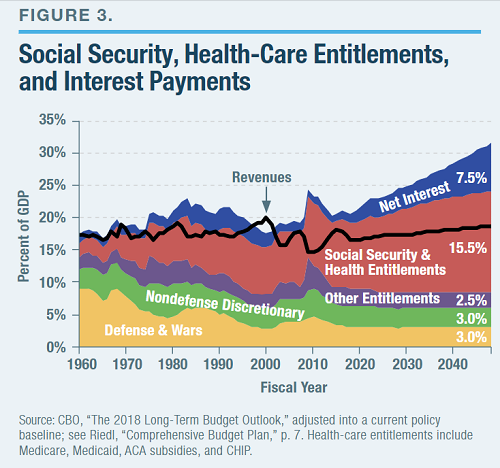

As to how the national debt can be addressed, the Manhattan Institute has some ideas.

Nearly all the projected growth in budget deficits over the next 30 years comes from Social Security and federal health benefits (particularly Medicare and Medicaid). Yet past deficit-reduction deals relied mostly on cuts to discretionary spending and payments to Medicare providers, which may not be able to sustain additional large reductions. Tax increases on the wealthy have played a modest role in past deals yet cannot fully close more than a small fraction of the fiscal gap. Most deficit reduction in coming years will need to come from entitlements—such as Social Security and Medicare (beyond more provider cuts)—that have often proved resistant to reform.

Budget deficits are set to exceed $1 trillion in the next year, on their way past $2 trillion within a decade if current policies continue. Over the next three decades, the Congressional Budget Office (CBO) forecasts $84 trillion in new deficits, which will bring the federal debt to 150% of GDP. And that is the rosy scenario—it assumes peace, prosperity, low interest rates, no new government programs, and the expiration of most of the 2017 tax cuts. More realistically, the debt could surpass 200% of GDP.While much has been written about the dangers of the ever-growing debt—and the need for a bipartisan “grand deal” to avert a fiscal calamity—the reality is that Congress and the White House are moving in the wrong direction. Republicans are cutting taxes, while Democrats are promising massive new spending.

There’s more at the link. Well worth reading, even if unlikely to succeed (because our partisan politicians simply won’t get down to business and work together, even on a project of such overwhelming national importance).

We clearly need a better class of politician, on both sides of the aisle.

Peter

Hey Peter;

As long as politicians can promise to deliver the "goodies" to a certain constituency he/she/it ain't gonna loose and demagogue the other side for any "cuts", it ain't gonna get fixed.

We never get better politicians until social Darwinism wipes out a goodly number of the idiots voting their avatar idiots into office.

What cannot continue, will not.

And then comes the die off, and the net increase in IQ among survivors.

We know, historically that stupid people die first, because stupid.

The humane thing would be to concentrate them, and accelerate this phenomenon.

Societal collapse does that marvelously, but it's also why civilization can't always have nice things.

Prepare for the coming Dark Ages.

1960 was the "Good Old Days", for most values of that which matter.

I expect better out of Prager U. That was pretty unimpressive.

There's a common meme that goes, "why is it I always hear about social security running out of money but I never hear about welfare running out of money?" We were required to pay into social security under penalty of imprisonment (if not worse when they come to arrest you). No one paid anything into "general welfare" and the one thing LBJ's "war on poverty" did was stop a 20 year downward trend in poverty and make it constant. Social security has been horribly mismanaged. After all "horrible mismanagement" is what government does best; or most often.

The aging of the population and the movement of baby boomers onto soc sec is probably the most predictable future expense there ever has been or ever will be, and yet government never once in the, oh, 60 years they've had available did anything to improve the situation. Did they bump the full eligibility age up a couple of years?

Denninger says social security is actually in pretty good shape. A couple of relatively small tweaks is all it needs. Medicare is the problem. And the fact that medicare even exists is part of the reason for its problems. The effects of a system that has no market feedback signals (the medical cost/payment system) with the "infinite checkbook" of the Fed.gov is to cause prices to go up at multiple times the consumer price inflation. Every place government gets involved, this happens. Look at college tuition due to the blank checkbook for student loans.

And all we get is Democrats without the slightest knowledge of the numbers saying, "Tax the rich!". If you took 100% of the income of the top 1% they always demonize, you could run the government a few months.

The problem is that debt doomsayers have been preaching the collapse of the US economy for 40 odd years (at least). So far it hasn't collapsed, and the major downturns haven't been due to federal government debt.

It is also clear that, while a rapidly increasing money supply can result in high inflation, there isn't a clear relationship between deficits and inflation. The high inflation of the 1970s had relatively small deficits. The 1980s saw large deficits with low inflation. The 1990s saw small deficits or surpluses with low inflation. Since 2000 we've seen large deficits with moderate inflation (yes, the numbers are fudged, but we aren't seeing hyperinflation as some predicted).

So it seems clear economists don't understand how deficits translate into inflation or economic collapse, at least for the economy which issues the world's reserve currency. If the US dollar loses its place or the US government has to borrow money in Euros or Yuan instead of dollars things might change.

I posted about how this works 6 years ago:

Well, the majority of it goes to so-called 'mandatory spending' and interest on the money that we have already borrowed. Mandatory spending includes entitlements like Medicare, Social Security, VA benefits, etc. which are REQUIRED by law to be paid. Interest on the debt must also be paid. The money that must be paid totals about $2.5 trillion a year. You get that? Social Security, interest on the debt, Medicare, and the like already total more than we take in through taxes.

https://street-pharmacy.blogspot.com/2013/09/spending.html

How to pay down an enormous debt –

1) Default. It's not like creditors can send for the sheriff.

2) Civil war, and the new government does not assume the debts of the old.

3) Massive inflation to minimize the impact of the payments.

4) Cut entitlements down to nothing, and pay it off over the next century.

Such a mess . .

*Cut expenses ~ if you didn't earn it/invest in it, you Don't get benefits from it!!

*Prepare for our creditors to come for payment/U.S. land in exchange for payment . .

*Prepare for our creditors to take over/divide up the U.S. in exchange for debt and we have to adapt to their laws~ can we win a war against multiple countries trying to collect debt by force?!!?

http://www.patreon.com/karenjoyce

Gee, name a country NOT in debt. Why is that? If I owe you and you owe him, I could pay him and we're all square. But that never happens. Ever wonder just WHO is it we owe? Ever have a look at who owns the federal reserve?

Look at

The creature from Jekyll Island

Listen to G.Edward Griffin on YouTube.

Learn about

Confessions of an Economic Hit Man.

If anyone ran their finances using the same rules the government does, they would go to jail.

Doesn't take a genius to know debt is bad..

Thanks for the education.